When making

large purchases, people generally like to shop around, compare deals and make

sure they're paying the right price. That could be for a car, a new computer, a

home warranty or a home mortgage. Most people don't rush into purchasing the

first one they see. The process of making sure you're getting the best deal can

take time and effort. Wouldn't it be great if you could have an insider give

you free advice on where to get the best deal? With a home mortgage, you can!

That insider is called a mortgage broker and they work with lenders to get you

the best deal for a mortgage. Landmark, a home warranty company, takes a closer

look into what a mortgage broker is and what they do.

What is a mortgage broker?

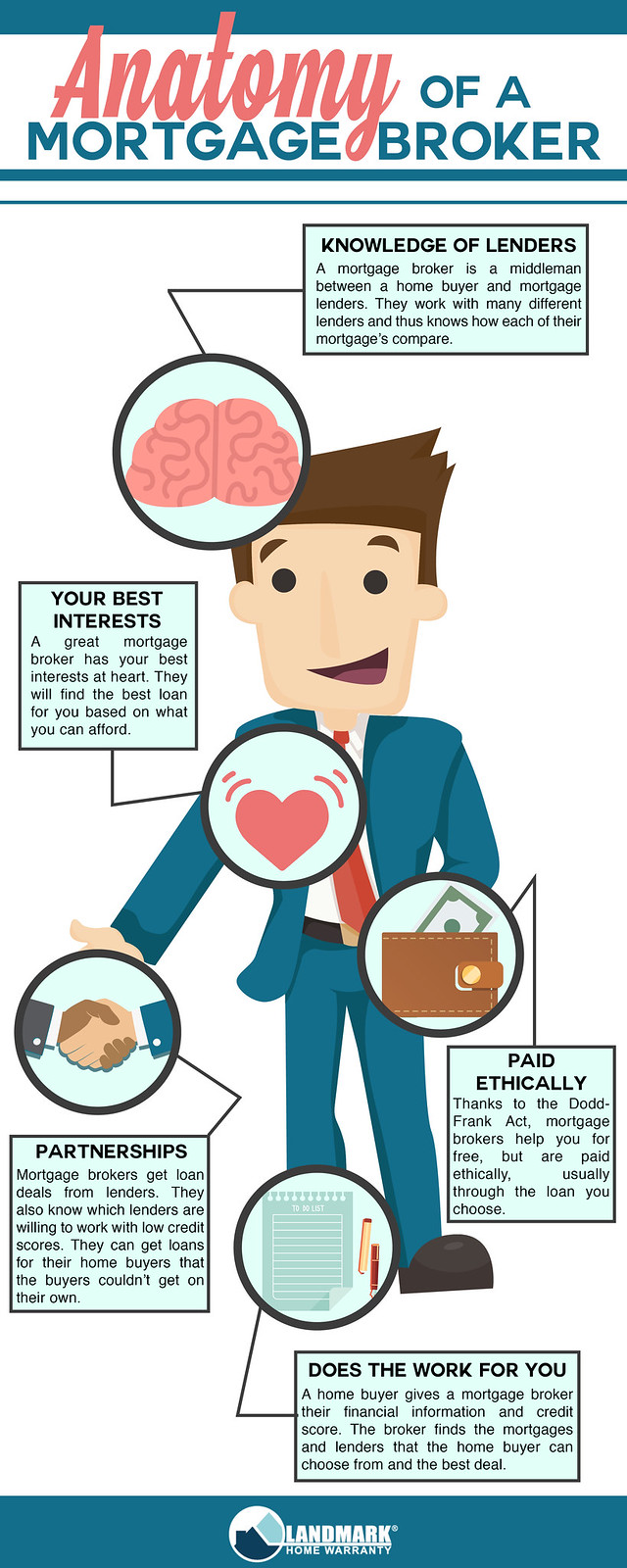

A mortgage broker is a middleman between a homebuyer and mortgage lenders. They work with many different lenders and thus knows how each of their mortgage's compare. As a buyer, you would provide the mortgage broker with your credit score and financial information and the mortgage broker will find the best lender for you and your financial situation. A mortgage broker will let you know what loan you qualify for and what you can afford. Of course, homebuyers could do this themselves, but it saves a lot of time and hassle to have someone with an insider-view do the legwork for you, especially when you don't generally have to pay them upfront. Mortgage brokers can also steer individuals away from lenders who have tricky contracts and payment terms. A mortgage broker works between the buyer and the lender throughout the entire loan process. This means they will find the loan that fits a buyer's needs for the home they want, and whatever the real estate transaction includes, like a home warranty or inspection fees. (Most of the time a home warranty will come with the home through a real estate transaction, however.)

Some buyers with

lower credit scores like working with a mortgage broker because they have

connections with lenders who will be willing to work with individuals who have less

than perfect credit. Other buyers like working with mortgage brokers because

they get loan deals from lenders because they have relationships with the

lenders. Some mortgage brokers also help homebuyers save money by elimination

appraisal and application fees for loans.

What is the difference between a mortgage broker and a loan officer?

Quite simply, a loan officer works for a specific lender and a mortgage broker has regular content with a large amount of lenders to get the best loan for your situation.

A loan officer

on the other hand works for one specific lender. If you choose to work with a

loan officer they will know how to get you the best deal on a mortgage in their

company, but can't compare those deals with outside of the lending office. A

loan officer writes the loans for their lending institution.

How is a mortgage broker paid?

Some buyers are

concerned about working with a mortgage broker because they assume they're

being paid based on the cost of the loan they sign. This is not true, and also

is illegal thanks to the Dodd-Frank Act. This act states that a mortgage broker

cannot be paid from your loan's interest or for signing a buyer up for a

specific lender. Instead, the mortgage broker is paid one to two percent from

the loan and is either paid by the buyer or by the institution- not both.

How do you choose the best mortgage broker?

There may be some brokers out

there who don't have your best interests at heart. Take your realtor's

recommendations. They will recommend a trusted mortgage broker, home warranty

company and inspector.

Landmark provides coverage for

systems and appliances within a home. A home warranty covers all of the major

electrical, plumbing, and HVAC systems inside of your home. A home warranty can

come with a home through a real estate transaction or put ona home that has

been owned for years. If an appliance or system breaks down from normal wear

and tear, a home warranty will pay to repair or replace the failed system or

appliance for a service call fee. For more information about getting a home

warranty for your home, go to Landmark's main page at www.landmarkhw.com.

References:

http://www.investopedia.com/financial-edge/1112/advantages-and-disadvantages-of-using-a-mortgage-broker.aspx

http://www.realtor.com/advice/mortgage-brokers-paid/

http://www.thetruthaboutmortgage.com/what-is-a-mortgage-broker/

http://www.zillow.com/mortgage-rates/buying-a-home/what-does-a-mortgage-broker-do/